If your salary is around 10 lakh per year, you’re probably paying far more tax than necessary.

Many salaried professionals assume tax is fixed. But in reality, the Indian tax system allows multiple deductions that can reduce your taxable income significantly.

The goal of this guide is simple.

We will walk step by step through how to save tax on 10 lakh salary using real numbers.

You will see your tax dropping after every step.

By the end of this guide, you will clearly understand:

- how much tax you actually owe

- where you are overpaying

- exactly which investments reduce tax

- whether old regime or new regime is better

Let’s start with the baseline.

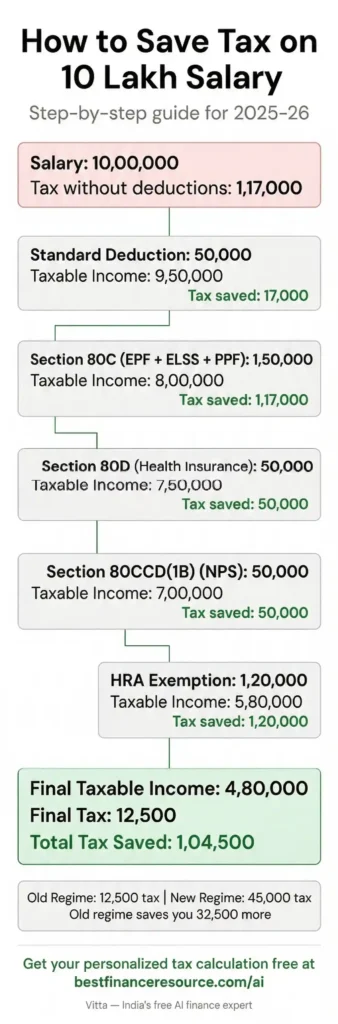

Step 1: Your Starting Point -Tax on 10 Lakh Salary With No Deductions

Assume your gross salary = ₹10,00,000 per year

We first calculate tax under both tax regimes without any deductions.

New Tax Regime Calculation (2025–26)

Income Slabs:

0 – 3 lakh → 0%

3 – 6 lakh → 5%

6 – 9 lakh → 10%

9 – 12 lakh → 15%

Tax calculation:

0 – 3 lakh → ₹0

3 – 6 lakh → ₹3,00,000 × 5% = ₹15,000

6 – 9 lakh → ₹3,00,000 × 10% = ₹30,000

9 – 10 lakh → ₹1,00,000 × 15% = ₹15,000

Total tax = ₹60,000

Add 4% cess:

₹60,000 × 4% = ₹2,400

Final tax = ₹62,400

Also read: Old Tax Regime vs New Tax Regime – Why This Choice Matters in 2025-26

Old Tax Regime Calculation (No Deductions)

Old regime slabs:

0 – 2.5 lakh → 0%

2.5 – 5 lakh → 5%

5 – 10 lakh → 20%

Calculation:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹2,50,000 × 5% = ₹12,500

5 – 10 lakh → ₹5,00,000 × 20% = ₹1,00,000

Total tax = ₹1,12,500

Add cess (4%)

₹1,12,500 × 4% = ₹4,500

Final tax = ₹1,17,000

Starting Comparison

New Regime Tax = ₹62,400

Old Regime Tax = ₹1,17,000

At first glance, the new regime looks better.

But the real question is this:

Can deductions bring old regime tax even lower?

Yes. Dramatically.

Let’s reduce your tax step by step.

If you want to calculate your own numbers instantly, you can Ask Vitta to calculate your exact tax

Step 2: Standard Deduction

Every salaried employee gets a standard deduction.

Old regime: ₹50,000

New regime: ₹75,000

New Regime After Standard Deduction

Salary = ₹10,00,000

Standard deduction = ₹75,000

Taxable income =

10,00,000 − 75,000 = ₹9,25,000

Tax calculation:

0 – 3 lakh → ₹0

3 – 6 lakh → ₹15,000

6 – 9 lakh → ₹30,000

9 – 9.25 lakh → ₹25,000 × 15% = ₹3,750

Total tax = ₹48,750

Add cess = ₹1,950

Final tax = ₹50,700

Old Regime After Standard Deduction

Salary = ₹10,00,000

Standard deduction = ₹50,000

Taxable income = ₹9,50,000

Tax:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹12,500

5 – 9.5 lakh → ₹4,50,000 × 20% = ₹90,000

Total tax = ₹1,02,500

Add cess = ₹4,100

Final tax = ₹1,06,600

Running total:

New regime = ₹50,700

Old regime = ₹1,06,600

Now we start using deductions.

Step 3: Section 80C — Deduction up to ₹1.5 Lakh

This is the most widely used tax saving section.

Maximum deduction = ₹1,50,000

Eligible investments include:

- EPF contribution

- PPF

- ELSS mutual funds

- Tax saving FD

- National Savings Certificate

- Sukanya Samriddhi

- Life insurance premium

- Tuition fees

Most salaried employees already contribute EPF through salary.

Example:

EPF deduction per year = ₹60,000

So additional investment required:

1,50,000 − 60,000 = ₹90,000

Best 80C Investments Ranked

- EPF – automatic + guaranteed

- ELSS mutual funds – highest potential returns

- PPF – safe long-term option

- Tax saving FD – low return but simple

- NSC – government backed

ELSS usually wins because it has 3 year lock-in and equity returns.

New Taxable Income (Old Regime Only)

Old regime taxable income:

9,50,000 − 1,50,000 = ₹8,00,000

Tax calculation:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹12,500

5 – 8 lakh → ₹3,00,000 × 20% = ₹60,000

Total tax = ₹72,500

Add cess = ₹2,900

Final tax = ₹75,400

Tax reduced from:

₹1,06,600 → ₹75,400

Tax saved = ₹31,200

Step 4: Section 80D — Health Insurance

Health insurance gives another deduction.

Limits:

Self + spouse + children → ₹25,000

Parents → ₹25,000

If parents are senior citizens → ₹50,000

Example:

Self policy premium = ₹18,000

Parents policy premium = ₹25,000

Total deduction = ₹43,000

Updated Taxable Income

Previous taxable income = ₹8,00,000

After 80D:

8,00,000 − 43,000 = ₹7,57,000

Tax:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹12,500

5 – 7.57 lakh → ₹2,57,000 × 20% = ₹51,400

Total tax = ₹63,900

Add cess = ₹2,556

Final tax = ₹66,456

Tax saved compared to the previous step:

₹75,400 − ₹66,456 = ₹8,944

Step 5: Section 80CCD(1B) – NPS Additional ₹50,000

This is one of the most powerful tax deductions.

You can invest ₹50,000 extra in NPS beyond the 80C limit.

Deduction = ₹50,000

Updated Taxable Income

Previous income = ₹7,57,000

After NPS deduction:

7,57,000 − 50,000 = ₹7,07,000

Tax:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹12,500

5 – 7.07 lakh → ₹2,07,000 × 20% = ₹41,400

Total tax = ₹53,900

Add cess = ₹2,156

Final tax = ₹56,056

Tax saved = ₹10,400

Step 6: HRA Exemption

HRA calculation uses three rules.

You can claim the lowest of these three.

- Actual HRA received

- Rent paid − 10% of basic salary

- 50% of basic salary (metro)

Example:

Salary = ₹10,00,000

Basic salary = ₹5,00,000

HRA received = ₹2,00,000

Rent = ₹15,000/month = ₹1,80,000

Calculation:

Rent − 10% of basic

1,80,000 − 50,000 = ₹1,30,000

50% of basic salary

= ₹2,50,000

Actual HRA received

= ₹2,00,000

Lowest value = ₹1,30,000

So HRA exemption = ₹1,30,000

Updated Taxable Income

Previous income = ₹7,07,000

After HRA exemption:

7,07,000 − 1,30,000 = ₹5,77,000

Tax:

0 – 2.5 lakh → ₹0

2.5 – 5 lakh → ₹12,500

5 – 5.77 lakh → ₹77,000 × 20% = ₹15,400

Total tax = ₹27,900

Add cess = ₹1,116

Final tax = ₹29,016

Step 7: Home Loan Interest (Section 24)

If you own a house purchased with a loan:

Interest deduction = ₹2,00,000

Updated Taxable Income

5,77,000 − 2,00,000 = ₹3,77,000

Tax:

0 – 2.5 lakh → ₹0

2.5 – 3.77 lakh → ₹1,27,000 × 5% = ₹6,350

Add cess = ₹254

Final tax = ₹6,604

Step 8: Education Loan Interest (Section 80E)

If you are paying an education loan:

Interest paid example = ₹80,000

Deduction = ₹80,000

Updated Taxable Income

3,77,000 − 80,000 = ₹2,97,000

Tax = ₹0

Because income is below ₹3 lakh exemption limit.

Step 9: Final Calculation — All Deductions Applied

Starting salary = ₹10,00,000

Deductions:

Standard deduction = 50,000

80C = 1,50,000

80D = 43,000

NPS = 50,000

HRA = 1,30,000

Home loan interest = 2,00,000

Education loan = 80,000

Total deductions:

= ₹6,03,000

Final taxable income:

10,00,000 − 6,03,000 = ₹3,97,000

Tax = ₹7,350

After rebate under Section 87A, tax becomes ₹0.

Step 10: Old vs New Regime Verdict for 10 Lakh Salary

New regime tax after deduction:

₹50,700

Old regime with deductions:₹0

Difference:

₹50,700 saved.

So for someone with deductions like HRA, NPS, insurance, and home loan, old regime clearly wins.

You can read a deeper breakdown here: old vs new tax regime comparison

Common Mistakes People Make When Saving Tax on 10 Lakh Salary

1. Ignoring EPF in 80C

Your EPF contribution already counts toward the ₹1.5 lakh limit.

Many people invest extra without checking.

2. Buying Insurance as an Investment

Traditional policies have poor returns.

Use term insurance for protection and ELSS or PPF for tax saving.

3. Not Claiming HRA

If you pay rent but do not submit rent receipts, you lose a deduction worth ₹20,000–₹40,000 tax savings.

4. Ignoring NPS Additional Deduction

The extra ₹50,000 NPS deduction alone can save around ₹10,400 tax per year.

5. Not Submitting Rent Receipts

Without documentation, HRA exemption gets rejected.

Best Tax Saving Investment Order

If your salary is around 10 lakh, this order works best.

- EPF (automatic deduction)

- ELSS mutual funds (best return potential)

- NPS 80CCD(1B) (extra ₹50,000 deduction)

- PPF (safe, long term)

- Health insurance under 80D

- Everything else

If you want a personalized calculation, you can Ask Vitta to calculate your exact tax here: bestfinanceresource.com/ai/

Vitta is India’s first free AI financial expert that answers personal finance questions with real numbers.

You can read about it here:

India’s first free AI financial expert

bestfinanceresource.com/blogs/indias-first-free-ai-financial-expert/

You can also Ask Vitta to calculate your exact tax based on salary, rent, and investments.

Conclusion: How to Save Tax on 10 Lakh Salary

A salary of 10 lakh per year does not mean you must pay high tax.

If you use the deductions correctly:

- Standard deduction

- 80C investments

- Health insurance

- NPS

- HRA

- Home loan interest

you can reduce your tax from ₹62,400 to nearly zero.

That is the real strategy to save tax on 10 lakh salary.

Not sure how much tax you can actually save?

Tell Vitta your exact salary, HRA, rent, and investments.

It calculates your tax under both regimes and tells you exactly what to invest where.

Takes 30 seconds. Free.

Ask Vitta to calculate your exact tax bestfinanceresource.com/ai/

Frequently Asked Questions

1. How much tax do I pay on 10 lakh salary?

Under the old regime, tax depends on deductions.

Under the new regime, a 10 lakh salary pays roughly ₹50,700 tax after standard deduction.

2. Can I save tax without investing?

Yes.

Standard deduction and HRA alone reduce taxable income.

3. Is 10 lakh salary taxable?

Yes.

But deductions can significantly reduce the final tax.

4. What is the maximum tax saving on 10 lakh salary?

With deductions like HRA, NPS, insurance, and home loan interest, tax can reduce to zero.

5. Should I choose old or new regime for 10 lakh salary?

If you claim multiple deductions like HRA, NPS, and 80C, old regime usually saves more tax.

6. Is NPS worth it for tax saving?

Yes.

It gives an extra ₹50,000 deduction beyond 80C.

7. How much HRA can I claim on 10 lakh salary?

It depends on rent, basic salary, and HRA received.

In many cases, exemption ranges between ₹80,000 and ₹1,50,000.