India’s income-tax administration has undergone rapid digitization over the past decade. E-filing rates have surged, compliance systems have become automated, and centralized processing has replaced many physical interactions. Yet recent government disclosures indicate that more than 24 lakh income-tax returns (ITRs) remain pending for processing.

The number has prompted questions about whether the backlog reflects systemic strain, compliance mismatches, or transitional challenges within India’s evolving tax infrastructure.

This article examines what the government has stated about the pending returns, how India’s ITR processing system works, and what broader trends in tax administration may explain the delay.

The Headline Figure: What Was Reported?

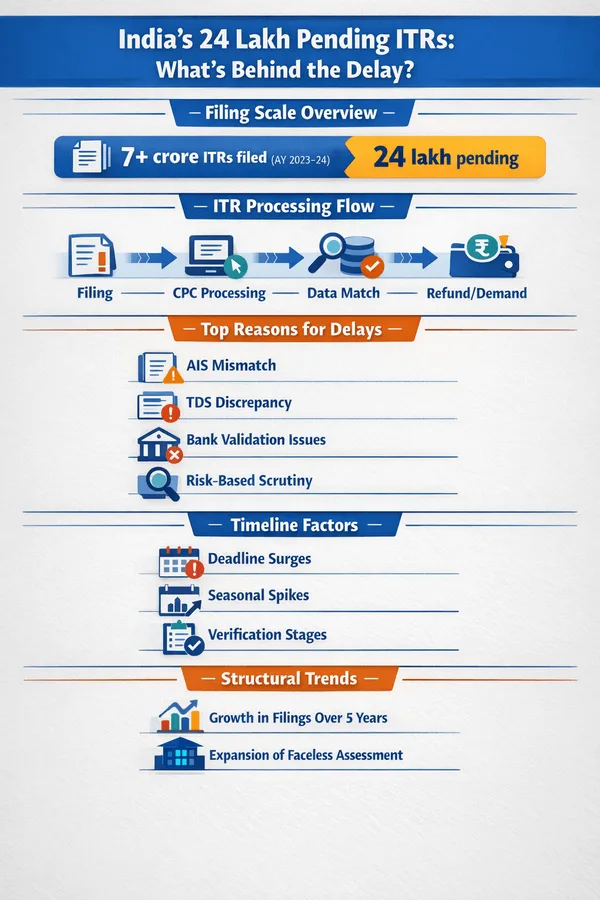

According to official disclosures in Parliament and subsequent reporting by government sources, over 24 lakh income-tax returns remain pending for processing for a recent assessment cycle. Such figures are typically released by the Ministry of Finance in response to parliamentary questions or through the Press Information Bureau (PIB).

India’s Central Board of Direct Taxes (CBDT) periodically publishes processing statistics through official communications and annual reports. For example, the Income Tax Department’s Annual Report 2022–23 highlights total returns processed and the proportion completed within specific timelines, reflecting improvements in automation and centralization.

Source: Central Board of Direct Taxes, Annual Report 2022–23

While millions of returns are processed each year, even a small percentage pending can translate into large absolute numbers due to India’s filing scale.

Also read: Complete Guide to Filing Income Tax Returns in India (AY 2025–26)

How Income-Tax Return Processing Works in India

To understand the backlog, it is important to distinguish between filing, processing, and refund issuance.

1. Filing

Taxpayers submit returns electronically via the Income Tax Department’s e-filing portal. Since the introduction of the revamped portal in 2021, digital filing has become the dominant mode.

Source: Press Information Bureau, Launch of New Income Tax e-Filing Portal (2021)

https://pib.gov.in/PressReleasePage.aspx?PRID=1727421

2. Processing

Returns are sent to the Centralized Processing Centre (CPC), primarily located in Bengaluru. Processing involves:

- Automated validation of income and deductions

- Cross-verification with TDS data (Form 26AS)

- Matching against Annual Information Statement (AIS) data

- Risk-based scrutiny flags

The system is largely automated, but certain returns are flagged for manual review.

3. Refund or Demand Notice

After processing, taxpayers may receive:

- A refund (if excess tax was paid), or

- A demand notice (if tax payable is identified)

The Income Tax Act mandates interest on delayed refunds under Section 244A, subject to certain conditions.

What the Government Has Said About the Delays

Government explanations for pending returns typically cite:

- Data mismatches between taxpayer declarations and third-party reporting

- TDS discrepancies

- Bank account validation failures

- PAN–Aadhaar linkage issues

- Returns selected for risk-based verification

India’s tax system increasingly relies on third-party data integration. Financial institutions, employers, and intermediaries report transactions that populate AIS and Form 26AS. When discrepancies arise between reported income and taxpayer-declared income, automated flags may delay processing.

The CBDT has repeatedly emphasized that a significant portion of returns are processed within days, but a subset requires additional verification.

Source: Income Tax Department, Time Taken to Process ITRs (Press updates, 2023)

https://incometaxindia.gov.in/Pages/press-releases.aspx

The Role of Automation and Risk-Based Scrutiny

India has expanded its faceless assessment system, introduced to reduce physical interface and increase transparency.

Source: Press Information Bureau, Faceless Assessment Scheme (2020)

The system uses:

- Data analytics

- Artificial intelligence tools

- Risk profiling

- Automated anomaly detection

While automation has accelerated processing for straightforward returns, it can also result in temporary holds when discrepancies are identified.

For example:

- High-value transactions reported by banks but not declared in the return

- Capital gains mismatches

- Large deduction claims requiring validation

Automation increases accuracy but may also increase flagging sensitivity.

Filing Volumes Are at Historic Highs

One structural reason for large pending numbers is the rapid growth in tax filings.

According to the Ministry of Finance, over 7 crore (70 million) income-tax returns were filed for Assessment Year 2023–24, marking continued year-on-year growth.

Source: Press Information Bureau, Record Number of ITRs Filed (2023)

India’s tax base has expanded significantly over the past decade. The Economic Survey 2022–23 highlights a steady increase in direct tax collections and return filings.

Source: Economic Survey 2022–23, Government of India

When filing volumes rise into the tens of millions, even a 3–5% verification rate may translate into several lakh pending cases at any given time.

Seasonal Bottlenecks and Deadline Surges

India’s tax calendar is heavily deadline-driven. A large proportion of returns are filed in the final weeks before the due date.

The Income Tax Department has reported that on peak days, millions of returns are filed within a 24-hour period.

Source: Press Information Bureau, ITR Filing Statistics Update (2023)

Such surges can temporarily strain backend systems, especially when:

- Revised returns are submitted

- Defective return notices are issued

- Technical corrections are required

Processing typically continues after the deadline, but high filing density can produce temporary backlogs.

Data Matching: A Key Source of Delays

India’s compliance framework increasingly integrates multiple reporting systems:

- Form 26AS: TDS and tax credits

- Annual Information Statement (AIS): Comprehensive financial transaction reporting

- Statement of Financial Transactions (SFT): High-value transaction reporting

AIS was expanded significantly in recent years to improve transparency.

Source: Income Tax Department, Annual Information Statement FAQs

If discrepancies arise between AIS data and declared income, processing may pause until clarification or system reconciliation occurs.

Common mismatch scenarios include:

- Employer TDS filing errors

- Bank reporting inconsistencies

- Capital gains computation differences

- Updated statements filed after the taxpayer submission

These systemic cross-checks improve long-term compliance but may temporarily slow individual return processing.

Portal Modernization and Transitional Challenges

In June 2021, India launched a new income-tax e-filing portal designed to improve user experience and backend integration.

Source: Press Information Bureau, New Income Tax e-Filing Portal Launched (2021)

Initial rollout challenges were widely reported, and the government acknowledged technical issues during early phases.

While stability has improved, large-scale digital transitions can produce processing delays, especially during data migration or system upgrades.

Refund Timelines and Interest Provisions

For taxpayers expecting refunds, delays can create liquidity uncertainty.

The Income-tax Act provides for interest on delayed refunds under Section 244A, calculated from the relevant assessment date until the refund is issued.

CBDT data from prior years indicates that a majority of refunds are processed within weeks for uncomplicated returns.

Source: CBDT Annual Report 2022–23

However, cases involving verification or discrepancy resolution may take longer.

It is important to distinguish between:

- Returns pending processing

- Returns processed but refunds under review

- Returns selected for scrutiny

Each category follows a different administrative pathway.

Structural vs. Temporary Backlogs

Backlogs can arise from two broad sources:

1. Structural Factors

- Growing taxpayer base

- Expanded data reporting requirements

- Risk-based compliance models

- Increased scrutiny of high-value transactions

2. Temporary Factors

- Deadline surges

- Portal updates

- Policy changes

- Technical reconciliation delays

The government has indicated in past communications that pending returns typically decline after reconciliation cycles are completed.

International Context: Digitization vs. Volume

India is not alone in facing processing surges during peak filing periods. Revenue authorities worldwide balance:

- Automation speed

- Data integrity checks

- Fraud prevention mechanisms

- Identity verification standards

India’s tax digitization push has been widely noted for scale and speed. The World Bank has referenced India’s improvements in digital tax systems in its Doing Business reports prior to their discontinuation.

Source: World Bank, Doing Business 2020 – India Profile

As data integration deepens, temporary processing friction can accompany increased enforcement precision.

Transparency and Public Accountability

Parliamentary disclosures serve as a mechanism for public oversight of tax administration performance. By releasing pending figures, the Ministry of Finance provides visibility into operational metrics.

Over the past decade, CBDT has increasingly published:

- Processing time statistics

- Refund volumes

- Direct tax collection data

- Compliance performance reports

This transparency aligns with broader administrative reforms under India’s tax modernization agenda.

What the 24 Lakh Figure Likely Reflects

Based on official explanations and structural trends, the pending return figure likely reflects a combination of:

- High filing volumes

- Data mismatch reconciliation

- Risk-based scrutiny flags

- Seasonal bottlenecks

- Backend verification processes

Given that annual filings exceed 7 crore, a backlog of 24 lakh represents a relatively small percentage of total submissions, though significant in absolute terms.

The Broader Modernization Story

India’s income-tax administration has undergone a major transformation since the introduction of:

- E-filing systems

- Centralized Processing Centres

- AIS integration

- Faceless assessment mechanisms

- Digital refund processing

Direct tax collections have also grown substantially, indicating expanded compliance.

Source: Economic Survey 2022–23

As systems mature, periods of processing friction may occur alongside improved cross-verification and enforcement capability.

Key Takeaways

- Over 24 lakh income-tax returns remain pending, according to recent government disclosures.

- The figure must be viewed in the context of over 7 crore annual filings.

- Delays often stem from data mismatches, verification flags, or reconciliation processes.

- Automation has accelerated processing for most returns but increased analytical scrutiny.

- Seasonal filing surges contribute to temporary bottlenecks.

- Transparency through parliamentary disclosures reflects administrative accountability.

India’s tax system continues to evolve toward deeper data integration and digital processing. While large pending numbers can draw attention, they often represent a transitional phase within a high-volume, technology-driven compliance framework.